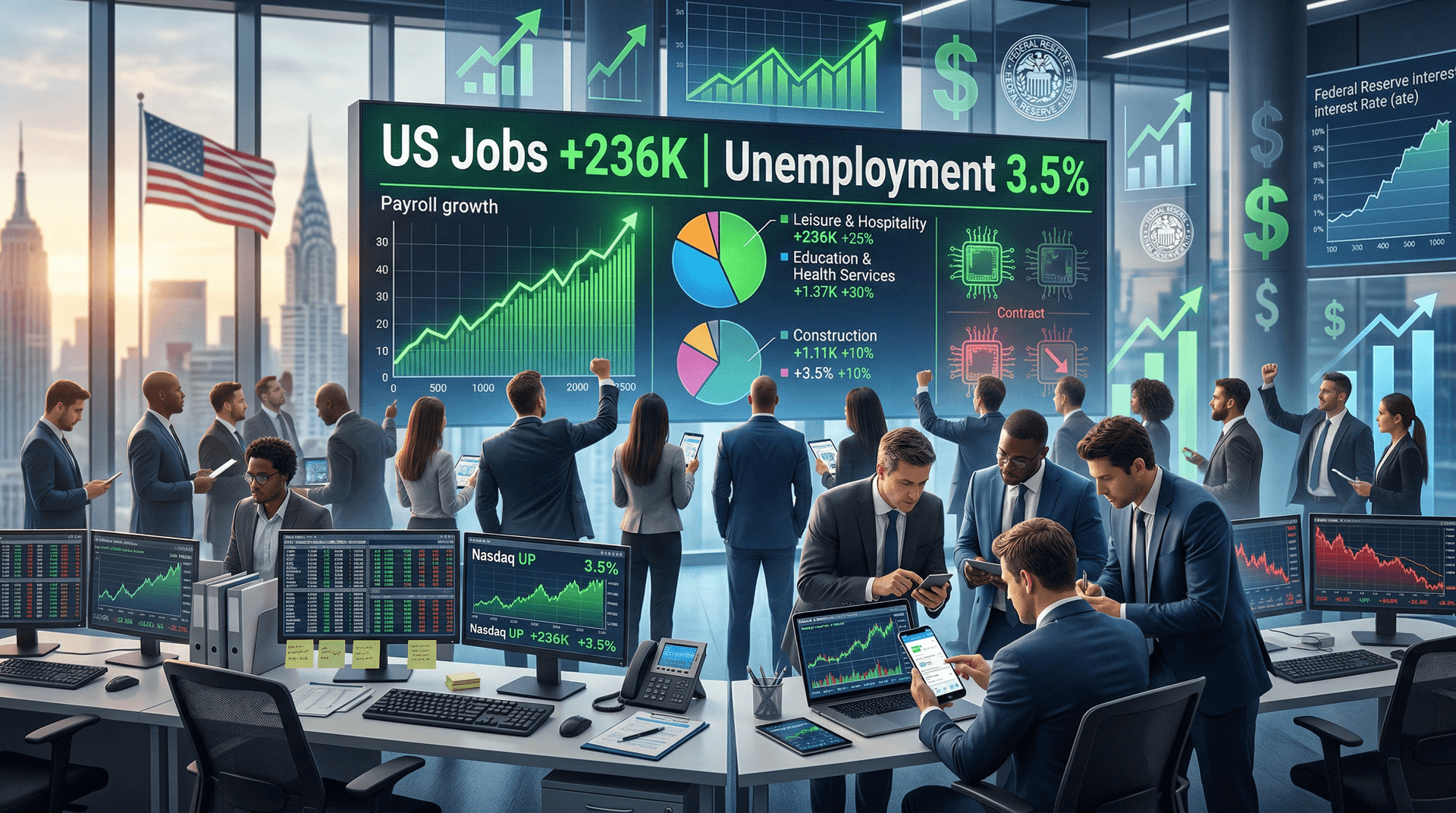

As a senior tech journalist covering the intersection of technology and finance, today's release of the March 2023 US jobs report by the Bureau of Labor Statistics (BLS) offers critical insights into the economy's health. Released on April 7, the data revealed nonfarm payroll employment surged by 236,000—a figure that exceeded Wall Street consensus estimates of around 228,000. The unemployment rate ticked down slightly to 3.5%, matching near-historic lows. This comes at a pivotal moment, with the tech sector grappling with aggressive layoffs while the overall labor market demonstrates remarkable tenacity.

Key Highlights from the Report

The report paints a picture of broad-based job growth:

- Total Nonfarm Payrolls: +236,000 jobs, revised upward from prior months.

- Unemployment Rate: 3.5%, with 5.8 million unemployed persons.

- Labor Force Participation: Stable at 62.6%.

- Average Hourly Earnings: Up 0.3% month-over-month and 4.5% year-over-year, signaling persistent wage pressures.

BLS Commissioner Julie Su noted in the official statement, "Employment continued to rise in March, with notable gains in leisure and hospitality, health care, and construction." These numbers suggest the regional banking turmoil from Silicon Valley Bank (SVB) and Signature Bank collapses in early March had minimal spillover into hiring trends.

Sector-by-Sector Breakdown

Diving deeper, job gains were uneven but predominantly positive:

| Sector | Change (in thousands) | |-------------------------|-----------------------| | Leisure & Hospitality | +49 | | Health Care | +40 | | Construction | +19 | | Transportation & Warehousing | +18 | | Retail Trade | -7 | | Professional & Business Services | -27 |

Notably, professional and business services—which includes IT and tech consulting—saw a net loss of 27,000 jobs. Computer systems design and related services shed approximately 9,000 positions. This aligns with the wave of cost-cutting in Big Tech: Meta announced 21,000 layoffs earlier in the year, Amazon trimmed 27,000 roles (including AWS), and Google cut 12,000. These moves reflect a post-pandemic recalibration after overhiring during the COVID boom.

Despite this, pockets of tech resilience persist. Software publishing added jobs, buoyed by demand for AI tools like OpenAI's GPT-4 (launched March 14). Cloud computing and cybersecurity firms continue selective hiring for specialized talent.

Wage Growth: A Double-Edged Sword

Average hourly earnings rose to $33.18, with a 4.5% annual increase outpacing inflation (CPI for February was 6%, latest available). This fuels concerns over a wage-price spiral, complicating the Federal Reserve's inflation fight. Tech workers, commanding premium salaries, saw even stronger gains—average IT salaries hover around $100,000+, per industry data. However, layoffs have softened bargaining power for some roles, potentially easing pressures in Silicon Valley.

Tech Sector in the Spotlight

From a tech perspective, the report underscores a dichotomy: macroeconomic strength versus sector-specific weakness. Tech employment has contracted by over 100,000 year-to-date, per Challenger, Gray & Christmas tracking. Companies like Microsoft and Salesforce paused hiring, citing efficiency gains from AI automation. Yet, venture capital into AI startups hit $3.5 billion in Q1, signaling hiring rebound in machine learning and data science.

The SVB fallout, tied heavily to tech startups, tested resilience. Over 90% of SVB deposits were uninsured, but federal interventions (including FDIC guarantees) prevented a credit crunch. Tech firms accessed emergency lines, sustaining payrolls. Looking ahead, expect tighter venture funding, pushing startups toward profitability over growth.

Immediate Market Reaction

Pre-market futures on April 7 pointed to gains: Dow Jones up 0.5%, S&P 500 +0.7%, Nasdaq +1.0%. Tech-heavy indices benefited, with Apple and Nvidia rising on job stability cues. Bond yields climbed, with 10-year Treasuries nearing 3.45%, reflecting rate hike bets. The report dilutes recession fears, supporting risk assets.

Twitter buzzed with analysts praising the "Goldilocks" scenario—not too hot, not too cold. Economists like Mark Zandi of Moody's Analytics tweeted, "Labor market cooling just enough to give Fed breathing room."

Federal Reserve Implications

Fed Chair Jerome Powell faces a delicate balance. Markets now price in a 25-basis-point hike at the May 2-3 meeting, with pauses later. Hot jobs data tempers soft-landing hopes but avoids panic. Powell's recent Jackson Hole echoes ring true: sustained 3.5% unemployment is "tight."

For tech, higher rates pressure growth stocks' valuations. Nasdaq's P/E ratio exceeds 25x, vulnerable to hikes. Conversely, steady jobs support consumer spending on gadgets—iPhone sales remain robust.

Broader Economic Outlook and Tech Hiring Trends

March's data revises February's payrolls up to 326,000 from 311,000, indicating sustained momentum. Revisions added 78,000 jobs over prior months, boosting confidence.

In tech, expect a bifurcated market: AI and cybersecurity boom, while generalist roles stagnate. Firms like Anthropic and Inflection AI ramp up amid GPT-4 hype. Remote work flexibility aids retention, but return-to-office mandates (Amazon, Google) spur talent mobility.

Globally, Europe's stagnant growth (UK jobs weak) contrasts US vigor, benefiting US tech exports. China's reopening adds tailwinds for supply chains.

Conclusion: Resilience with Caveats

This jobs report is a resounding endorsement of US economic fortitude, even as tech navigates turbulence. For investors, it's a buy signal for diversified portfolios; for tech leaders, a reminder to prioritize efficiency. As April unfolds, watch ISM services data and CPI (April 12) for confirmation. The labor market's strength offers breathing room, but inflation vigilance remains paramount.

In tech-finance nexus, March's numbers affirm: innovation drives jobs, but discipline sustains them.

Word count: 912